by Stuart Burgess

The mining industry is reliant on a robust pipeline of new discoveries, and this is the critical role that mineral exploration fills. Exploration, at its core, is a high-risk, high-reward venture that relies on a significant amount of trial and error, timing and luck – not to mention a healthy budget. In this column, let’s take a look at how the exploration landscape has changed over the last five years and the states where this shift has perhaps been the most evident.

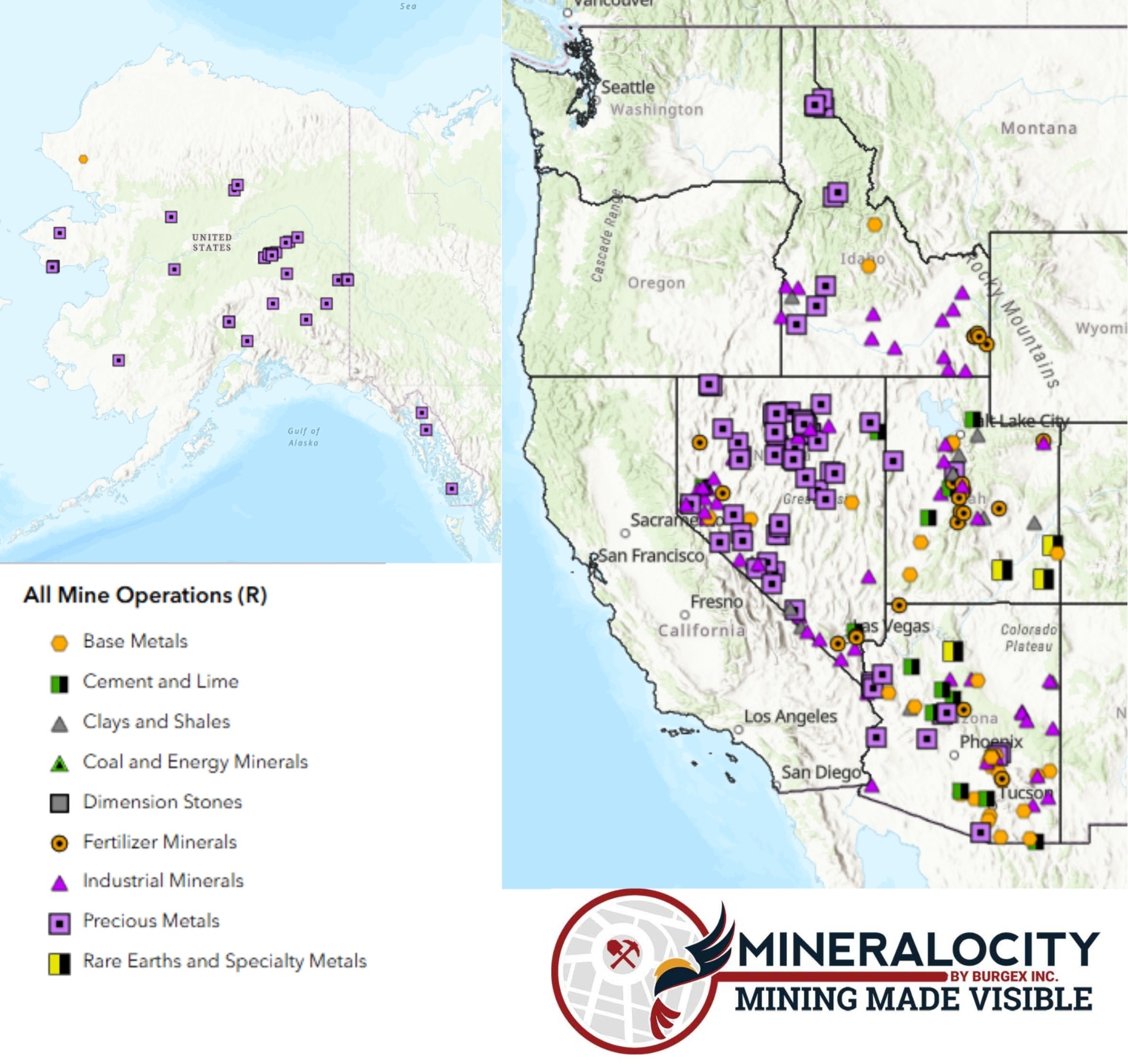

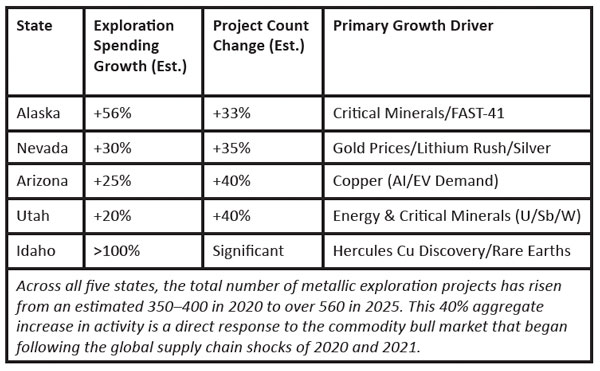

At the heart of this “States of Exploration” analysis is the quantification of activity within five primary hubs of domestic mineral discovery: Nevada, Arizona, Alaska, Utah and Idaho. These states represent the vanguard of a robust national effort to mitigate an expanding reliance on foreign mineral imports. According to the USGS, net imports of processed metals and materials more than doubled in value from $77 billion in 2024 to $185 billion in 2025, underscoring the urgency of developing a secure exploration pipeline. The narrative of modern exploration is increasingly split on a global scale; while grassroots exploration budgets internationally reached a record low of 22% in 2024, the United States has seen a significant uptick in late-stage and mine-site exploration, as major companies prioritize the de-risking of existing assets.

The current state of exploration cannot be decoupled from the macroeconomic volatility of the 2020–2025 period. Gold has emerged as a primary driver of activity, with prices surging 27% to $2,625 per ounce by the end of 2024 and continuing an aggressive ascent to reach $4,325/oz. by the end of 2025 – with further climbing and volatility so far in 2026. This rally, rooted in geopolitical tensions and central bank hedging, has translated into an 11% increase in gold exploration budgets to $6.15 billion globally. For the top U.S. states, this has resulted in a renewed focus on historic districts and smaller deposits that were previously considered marginal.

Simultaneously, the “critical minerals” movement has fundamentally altered the U.S. permitting and investment landscape. The Energy Act of 2020 and subsequent federal directives have prioritized 50 minerals essential to national security, including lithium, cobalt, tungsten, antimony and rare earth elements. While lithium exploration budgets faced a 46% decline globally in 2025 due to temporary oversupply and price moderation, the long-term outlook remains dominated by the transition to electric vehicles and renewable energy storage.

Nevada: The Silver State’s dominance in gold and lithium

Nevada remains the premier jurisdiction for mineral exploration in the United States, consistently taking the lead in non-fuel mineral production value. Much of Nevada’s exploration narrative is defined by its world-leading gold production, which accounted for approximately 70% of the U.S. total in 2024. Five years ago, Nevada’s exploration activity was largely a story of precious metals. In 2020, Nevada’s production value was approximately $9.14 billion, second to none in the U.S.

Since then, the transition has been a rapid expansion into the lithium sector as well as a renewed interest in the Silver State’s namesake. Nevada currently hosts 33 of the 50 federally designated critical minerals in some stage of exploration or development. Projects like Thacker Pass in Humboldt County – the largest lithium deposit in North America – have moved from exploration and permitting into the early stages of production and expansion.

Arizona: Copper porphyries and the AI-driven demand surge

The state is the absolute leader in U.S. copper production, accounting for over 70% of domestic output. The exploration sector in Arizona is currently experiencing a “perfect storm” of demand, as the dual pressures of the energy transition and the burgeoning Artificial Intelligence (AI) sector – which requires massive copper-heavy power infrastructure – drive exploration budgets to new heights.

Arizona, while also having its share of lithium, gold, and critical minerals exploration, continues to be heavily focused on copper. Major developments in 2025 include the advancement of the Santa Cruz copper project and record drilling at the Sugarloaf Peak gold project, which recently confirmed the lateral expansion of its deposit.

Alaska: The frontier of global mineral potential

Alaska presents perhaps the most dynamic exploration environment in North America. In 2024, the state was ranked first globally for mineral potential by the Fraser Institute. Despite high operating costs and infrastructure deficits, exploration spending in Alaska reached $250 million in 2024, an increase of approximately 56% compared to the levels seen five years ago.

Currently, there are approximately 60 active exploration projects in Alaska. Unlike Nevada and Arizona, where exploration is concentrated in known trends, Alaskan exploration is highly diversified across a range of high-value polymetallic and critical mineral deposits

Estimated Alaska exploration project breakdown (2024):

- Volcanogenic Massive Sulfide (Polymetallic): 36%

- Intrusion-related Gold: 32%

- Gold (Other types): 14%

- Graphite: 5%

- Porphyry Copper: 3%

- Mafic-UM Intrusion (Ni-Cu-Co-PGE): 3%

- Other (Rare Earths, Antimony, Lithium): 7%

Utah: Industrial stability and energy mineral resurgence

Utah represents a blend of industrial-scale mining and a burgeoning energy mineral sector. Historically centered on the Bingham Canyon copper mine, Utah consistently ranks in the top 10 states for production value of non-fuel minerals. Most of the base and precious metals production has historically come from Bingham Canyon, with minor production by others.

Exploration activity in Utah remains consistently active, particularly in counties such as Salt Lake, Tooele, Juab, and San Juan. A significant trend over the last five years has been the resurgence of interest in vanadium and uranium exploration as the U.S. seeks to secure its nuclear fuel cycle. Utah has also seen a boom in critical minerals exploration, with companies seeking to develop mines for antimony, fluorspar, beryllium, lithium and tungsten.

Idaho and the high-grade rare earth frontier

Idaho has rapidly moved into the spotlight as a critical jurisdiction for Rare Earth Elements (REEs), while also seeing a 100%-plus surge in exploration spend following the transformational discovery of a porphyry copper system at the Hercules property. The Lemhi Pass and Diamond Creek districts, which straddle the Idaho-Montana border, contain some of the highest-grade neodymium (Nd) deposits in the world.

Exploration in Idaho is not just about finding minerals; it is about finding grade. While soil in northern China contains 0.024% REEs, soil analysis from central Idaho has revealed concentrations exceeding 1.1%. This represents a potential paradigm shift for the U.S. rare earth supply chain, which is currently dependent entirely on Mountain Pass in California.

Five-year comparison of exploration trends

When contrasting the current “States of Exploration” with the landscape of 2019–2020, three distinct themes emerge: the critical mineral pivot, the price-induced gold expansion, and the permitting-to-production bottleneck.

Future outlook (2026 and beyond)

Looking ahead to 2026, the S&P Global World Exploration Trends report anticipates a rebound in financing for junior explorers, particularly as interest rates stabilize. Copper, silver and gold are expected to buoy exploration budgets, while the battery metal sector (nickel, cobalt and lithium) may see a recovery in investment as market surpluses are absorbed.

The quantitative and qualitative data for Nevada, Arizona, Alaska, Utah and Idaho paints a picture of an industry stepping into high gear. The exploration pipeline has expanded by nearly 40% in five years, driven by a strategic imperative to secure domestic supply chains and capitalize on record-breaking precious metal prices. While the U.S. still faces structural hurdles in moving these discoveries through the permitting phase, the “States of Exploration” are proving that the geological potential of the United States remains a foundational pillar of the global economy. For those of us out there kicking rocks in the field, the message is clear: the exploration landscape of today is more diversified, more valuable, and more essential than it has been in a generation.

Stuart Burgess is the Co-founder and Chairman of Burgex Mining Consultants. A specialist in mineral exploration and landman work, Stuart has spent his career bridging the gap between geological discovery and the complex regulatory landscape of the American West.